The inflation rate is a measurement of the average cost of items which is closely monitored by the Department of Stats. The price movements of around 400 items are measured to establish the annualised inflation rate. The rate is watched closely by the Reserve Bank which is mandated to keep it in a range of 3% to 6%. One of their mechanisms used is the adjustment of the interest rate to either stimulate or contain the economy.

Where is inflation heading?

Rising oil prices are beginning to erode the value of our money once again. After the surprising fall from last year, the price of oil seems to have bottomed out and is rising once again. The problem is compounded by a weaker rand as the price of oil is quoted in US Dollars, a currency which has significantly strengthened in the same period.

-R10.68 in August 2014 to R12.20. The price of oil was $113 per barrel at R10.68 in August 2014. At present it is $62 per barrel at R12.20.

Our inflation rate has nudged upwards already from 3.9% to 4.0% as a result of the rebound of the oil price and is set to rise even further in the face of rising costs of electricity and food.

Why is contained inflation important?

Well, simply put, it affects the value of your money. If something costs R100 today and inflation is 6% then in 12 years the same item will cost R200 which is double. If inflation is 12% then the same item will cost R200 in 6 years which is half the time.

The higher the rate of inflation the less your money is worth in the future.

What can we do about it?

Get rid of your debt

If inflation rises then interest rates will probably go up. This means that your debt will cost you more.

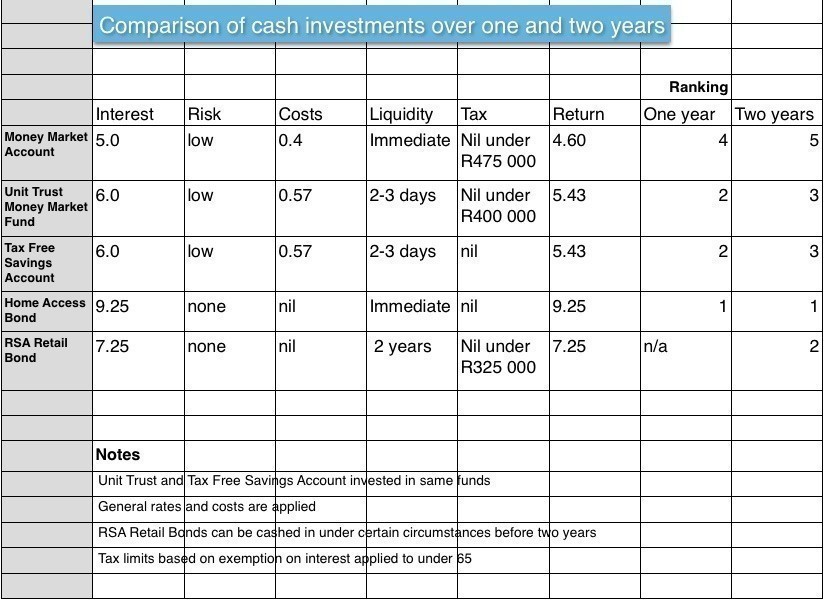

Invest in inflation-beating returns

Your returns should be above the inflation rate if your money is to stay real in the future.

Contain your spending

Inflation is driven by consumer spending. Curtailing your spending will keep more money in your pocket which can be used to pay off debt and improve your savings.